High Potential Startup #10: Plum

Group Employee Health Insurance for Small Companies

At time of publication: Series A | Total Funds raised 21mn USD

******

Millions in India are pushed into poverty each year due to medical expenses.

India has one of the lowest health expenditures per capita.

The Government health expenditure (center + state) as a share of GDP is far lower than other countries.

And the insurance penetration in India is very low. It is estimated that only 18% of Indians in urban areas and 14% of Indians in rural areas are covered by health insurance.

What effectively happens is most people cannot afford the care they need and still need to pay most of the expenses (58%) out of their pocket.

One of the efforts by the Government in the last few years has been to offer a standardized universal health insurance scheme that provides a basic cover (~$7000) targeted towards 107mn poor families. Over 160mn individual cards have been issued so far under the scheme. A key limitation is the focus on hospitalization - outpatient care is not covered though it contributes to 60% of out of pocket expenses. Overall though this is a step in the right direction.

But a lot more people need health insurance and coverage outside the poor sections of the society is also very low.

This is where Group Health Insurance offered by employers can play a key role in increasing coverage. Group health insurance, though probably less comprehensive than individual insurance, is paid by the employer and provides a basic health cover that is invaluable to many. Group insurance also has no waiting period and does not require medical checkups.

Typically insurers are willing to underwrite and process Group Insurance for large companies. The underwriting is better if there is a large group to spread the risk and the operational costs per person becomes viable. But in India, a huge majority of the population outside of agriculture is employed in micro, small and medium enterprises (MSMEs). What effectively has happened is many MSMEs cannot purchase affordable health insurance since many insurers are not interested to pursue this segment. Startups that innovate here hence can capture a massive market!

Plum is a startup that is tackling this problem. It offers Group Health Insurance to companies with employee count as low as 7 employees.

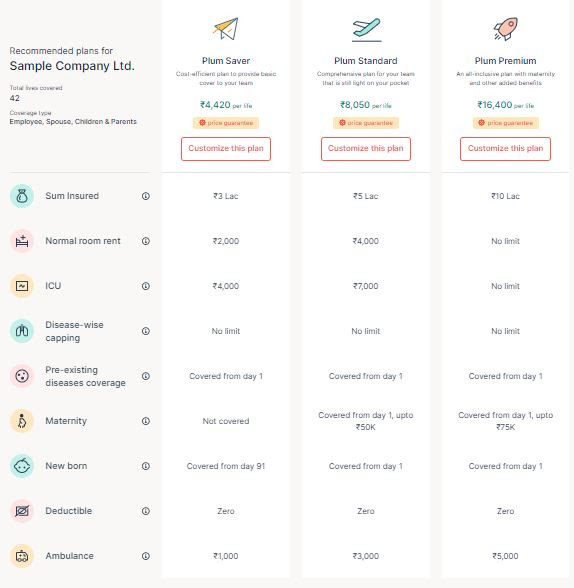

Plum Insurance partners with insurance companies to co-create insurance products for small companies. A small business owner can get a quote within minutes by answering a few questions on the website.

Screenshots from Plum

There are three coverage plans provided under ‘Plum Saver’, ‘Plum Standard’, ‘Plum Premium’ plans. These plans can further be customized and pricing is provided real time.

This is a fantastic experience delivered in minutes compared to waiting for days and weeks, which is usually the norm with legacy insurers.

Employees get a digital mobile ‘health card’ once onboarded that they can use to claim care.

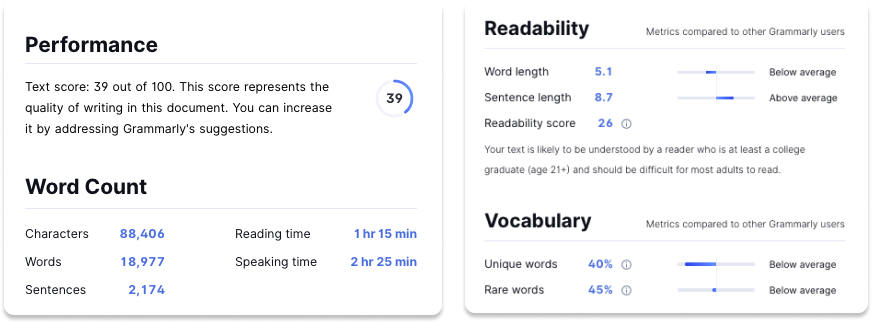

Plum also claims to strive towards high transparency and simplifying the understanding of insurance policies for employees. Here is a counter example (provided by Plum) of an analysis (via Grammarly) of a sample legacy insurance policy document which takes more than an hour to read and uses a lot of jargon.

The admin experience to manage employees is simple and intuitive.

The claims process is also quite simple where the employee can easily add bills and documents and there is round the clock chat support with a customer service rep.

The great user experience shows results. Plum Insurance sits at an Industry leading Claims NPS (Net Promoter Score) of 79.

Plum last year got a massive regulatory tailwind boost from the Government of India’s mandate to employers to provide medical insurance to employees.

Plum Insurance has become a veritable rocketship in the past year signing more than 600 companies (as of May’21). It announced recently that it has more than 100,000 members on the platform - 20x YoY and 110% Q-o-Q growth! The company notes 82% of organizations are first time insurance buyers.

As noted earlier, with the majority of the population employed in MSMEs and with regulatory mandates, there is massive headroom for growth in such a large market.

A quick glance at the companies onboarded to Plum show a massive list of new-age tech startups as customers.

A lot of these customers are startups that scale fast and add headcount at a fast clip and hence Plum can grow very fast as these startups scale.

One bugbear of digital insurance startups is the expensive search keywords and hence the high customer acquisition costs (CAC). The B2B2C approach of Plum Insurance ensures a low CAC. In fact, Plum claims 70% of the customers are via word of mouth.

Plum has partnered with leading health insurance companies. It also offers a white label solution for insurers. As it acknowledges:

“We cannot exist in a silo, we have to work with multiple ecosystem partners including insurance companies, payment processors, payroll providers, HR information systems & health benefits providers. One of our core strengths is that we build integration rails with our partners that create end-to-end workflows.”

Plum can also form wellness/fitness partnerships for employees and possibly integrate health/fitness data at the company level in the future that may reduce premiums for companies (which the companies can in turn use to incentivize/reward employees)

The product velocity is very impressive. Recently, they launched Teledoc, an in-house doctor telemedicine (consultations) service.

There are some hard insurance challenges like Underwriting and Fraud that Plum can continue to innovate and improve on with more data and more partnerships.

To summarize: Plum addresses an important problem for a highly underserved customer segment (82% of its customers are first time insurance buyers) in a very large market with great customer experience in an industry that is long due for change. It also has a massive regulatory tailwind that it is poised to capitalize on. Its product approach is to challenge fundamental assumptions and rethink how Group Insurance is created, delivered and administered. The B2B2C (and partnerships) approach means low CAC. Plum is a High Potential Startup to watch out for.