High Potential Startup #35: Tally

High Potential Startup #35: Tally

Helping pay off credit card debt faster

At the time of publication: Series D | Total funding raised: 172mn USD | Valuation: 855mn USD

*****

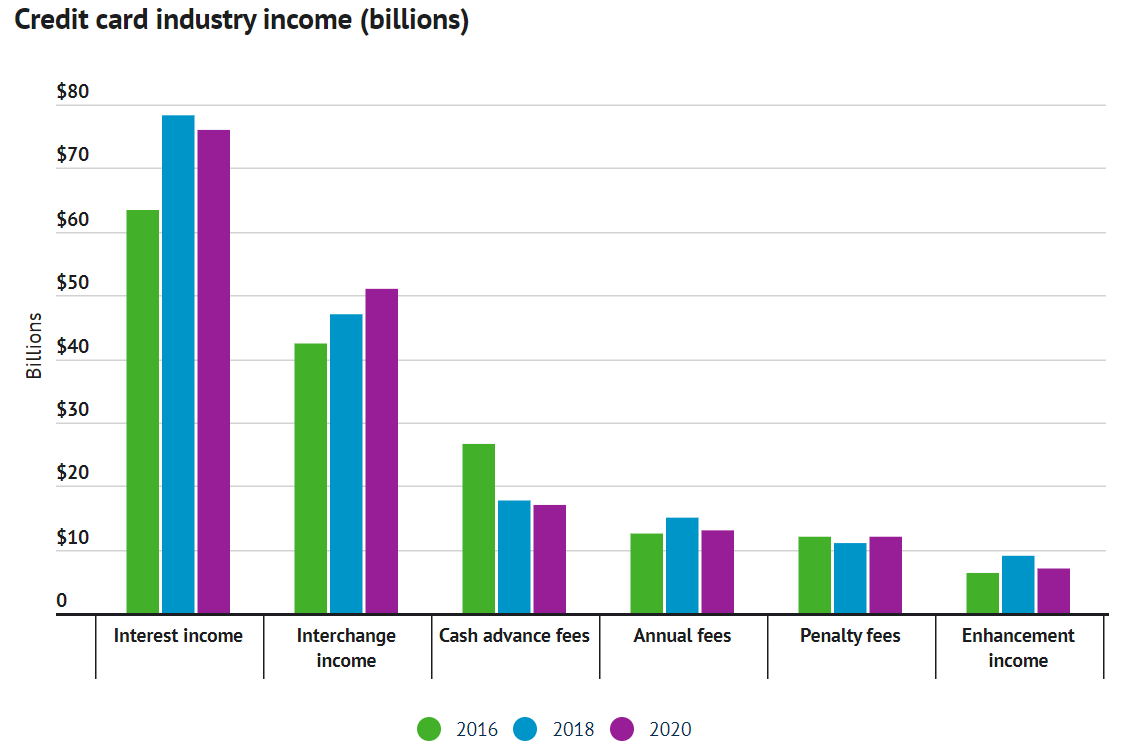

Credit card companies make most of their money not from the interchange fees they charge merchants but from interest rates paid by consumers. In 2020 for example, total credit card revenue in the US was 176bn$ out of which interest income was 76bn$.

And the interest rates on credit cards are absolutely exorbitant. The average interest rate on credit cards is a whopping 21% p.a. in the United States. Total loan balances are around 930 billion dollars in the country.

But here is a question - do these very high interest rates accurately reflect their risk?

Tally is a US based fintech startup that aims to reduce or clear off credit card debt for consumers.

Tally's core thesis is that credit cards charge way higher interest rates than they should for many consumers. If rates are even a few percentage points lower, then the consumers see real monthly savings in debt repayments and can pay off their debt much faster.

This is how it works

1. Customers combine all the cards they have in Tally (on average there are 4 credit cards per person in the US) and Tally determines the risk with a single view

2. If eligible, Tally calculates and provides the customer with a lowest interest rate credit line and the interest rate is typically much lower than what customers pay on their credit cards. (Tally algorithm calculates the interest rate basis credit score, balances, spending behavior and other factors)

3. If the customer accepts the credit line, then Tally immediately proceeds to pay off the existing credit card debt

4. The customer then repays Tally every month but now at a lower interest rate

For example, in one scenario if we take the average household credit card debt (roughly $9000), then customers can save around $1396 or repay the debt 5 months earlier.

Tally charges a $300 annual fee to access a higher credit line (‘Tally+ Membership’). This might be useful to pay off a larger credit card debt. This fee is added to the statement and the customer does not have to immediately pay out of the pocket.

The credit line is a revolving one and can be used for 'unlimited refills'. Once regular repayments are made, Tally lowers APR over time and this also helps in improving credit score for customers.

This is a great solution to a serious pain point and can save significant money for users. Tally co-founder and CEO Jason Brown says,

“Credit cards are designed to trap people in a cycle of debt… Our debt-free system helps consumers pay off credit cards faster, empowering them to take control of their finances and make real progress towards their financial goals.”

Fundamentally, while credit card companies make money when people don’t pay on time, Tally makes money when it helps people reduce their debt. It also has a ‘late fee protection’ and auto-pays money on your behalf on cards that charge you late fees. Interestingly, Tally compares itself to Costco which passes on savings with increasing scale.

If a user does not want to accept a credit line, they can still use Tally’s debt planning features.

Tally has seen very good traction and claims to have paid off more than $1bn in credit card debt with annual recurring revenue tripling over the past year. It makes its money from the interest rate it charges and the annual fees.

With interest rates and inflation rising, the credit card problem is going to become worse and more users will need Tally. Tally’s capabilities can extend to other high interest debt like student loans (which are bigger than credit card debts) in the future.

Tally recently raised money at a sizeable valuation of $855mn but considering the importance and size of the problem, the value Tally creates for its customers and its tech capabilities, there is very high future potential for Tally.